|

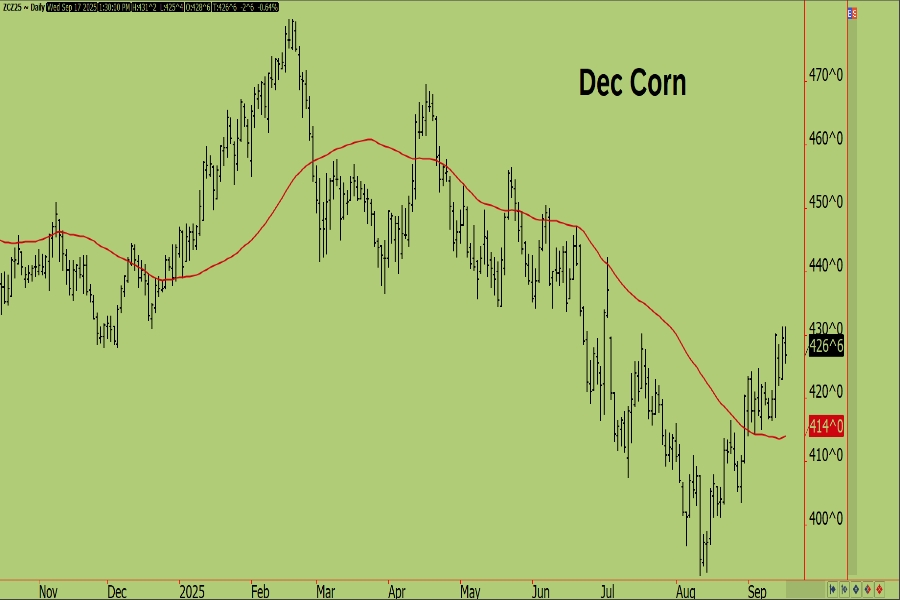

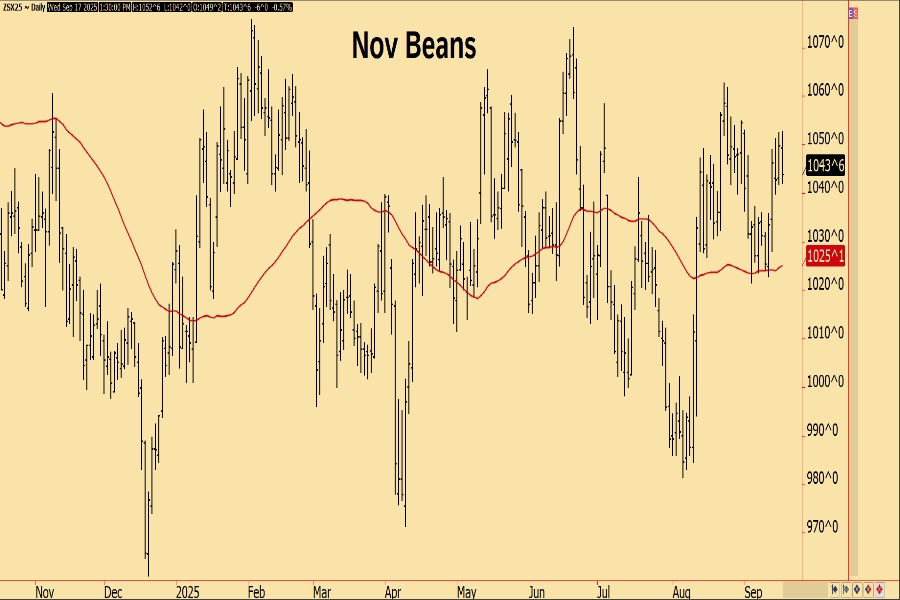

Ag markets in Chicago drifted to lower closes on Wednesday, led to the downside by the bean oil market which gave back all of what it gained on yesterday's EPA news and then some. Traders quickly realized between yesterday and today that while there's a chance 100% of the previously waved small refinery exemptions get passed on to larger refiners, there also exists, though maybe not at equal odds, a similar chance that 0% of these exemptions get passed on, which produced today's sell-off. In either case, a final ruling does not feel any much closer today than it did yesterday, which means bio and renewable fuel producers are likely to keep operating in the dark for the foreseeable future despite sharp futures price reactions the last couple days.

|