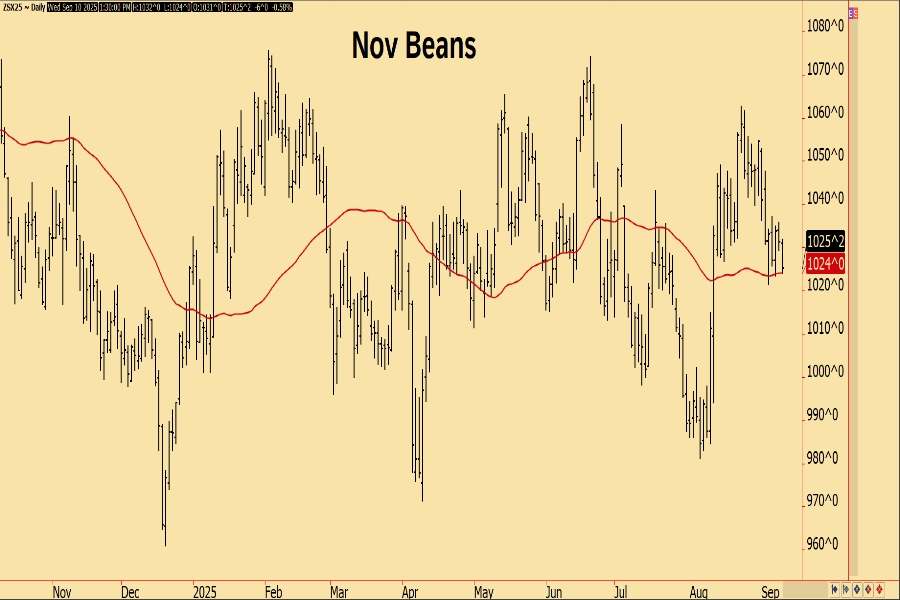

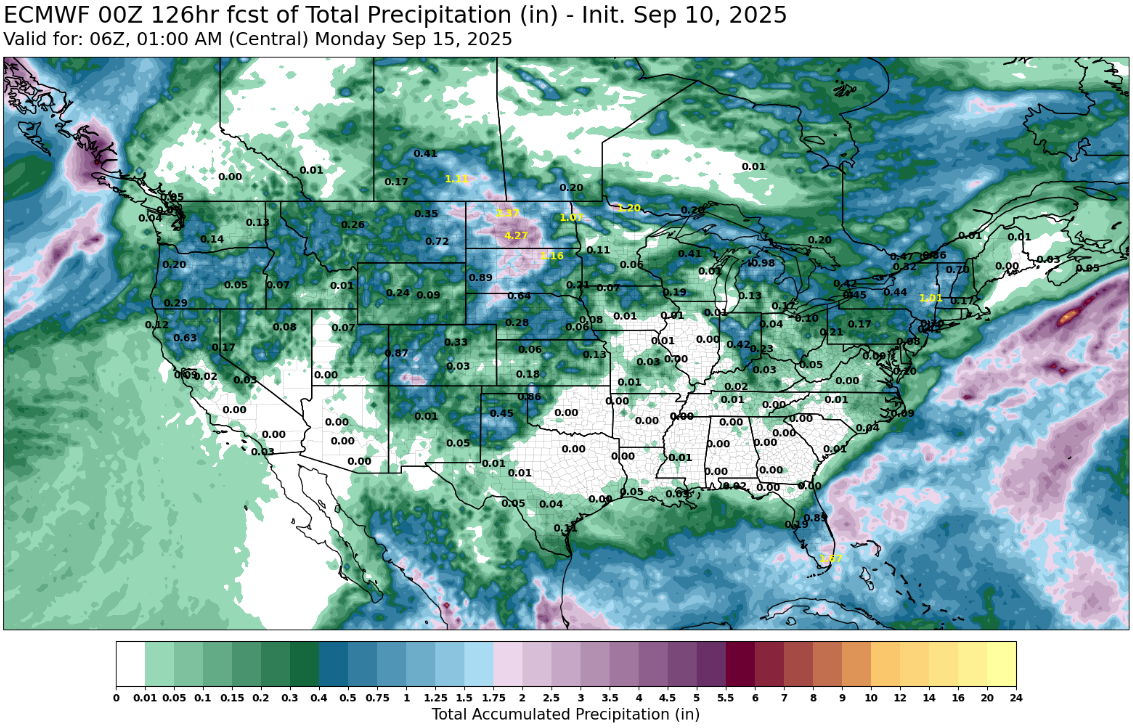

|

? Prices:

- December Corn (CZ): $4.17, down 2 3/4 cents

- March Corn (CH): $4.34 1/2, down 3 cents

- December/March Spread (CZ/CH): -17 1/2, up 1/4 cent

? Market Headlines:

- This morning's weekly ethanol report from the EIA with data for the week ending September 5th showed average daily production in the week at 1.105 mil bbls, which was up 2.8% from last week and up 2.3% from the same week last year. Corn usage in the week was estimated at 109.2 mil bu.

- Ethanol stocks were seen at 22.837 mil bbls, which was up 1.2% from the week prior but down 3.7% from the same week last year. This was also a new 5-week high stocks figure.

Summary:

Weekly ethanol data from the EIA this morning was positive, but other than that, Wednesday trade was almost identical to Tuesday's trade as there continues to be little excitement with harvest still not quite rolling. We've said it all month now but amid the wide-ranging yield debates that have occurred since the August crop tour season came and went, there is added uncertainty as to what is actually out in fields this year and this has produced a wait-and-see trading environment that has turned dull and uneventful quickly. Newswires reported today that total volume in the corn market was less than that of the bean oil market, further illustrating the lack of desire by most anyone to trade corn futures in the current scenario.

|