|

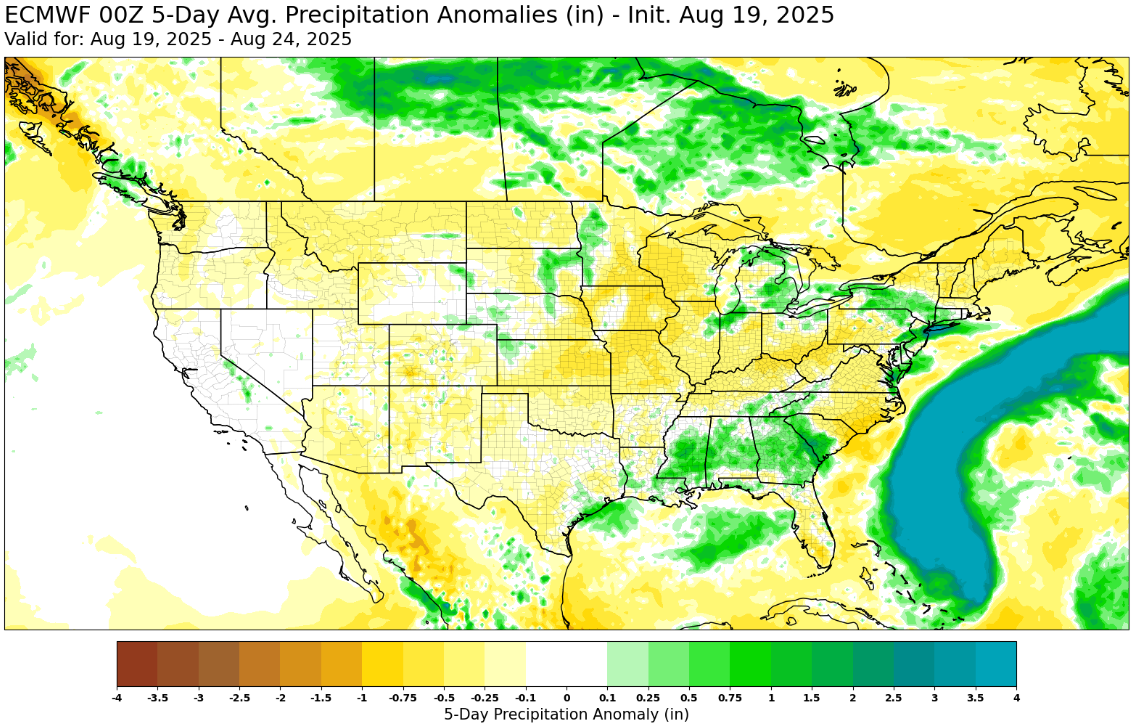

Chicago ag markets saw mostly lower trade throughout the day on Tuesday, with spread activity in the products able to lift meal to the only higher close for the group while corn, beans and wheat all fell to closes in the red. For a second day in a row, the Pro Farmer crop tour largely dominated the news cycle, though social media reports coming out through the day today would seem to indicate a crop that was a little rougher looking than what was seen yesterday, despite the markets trading lower. As is the case most years in August/September, trade direction is simply all about supply right now and we don't see this changing until combines start rolling or a China trade deal is announced.

|