|

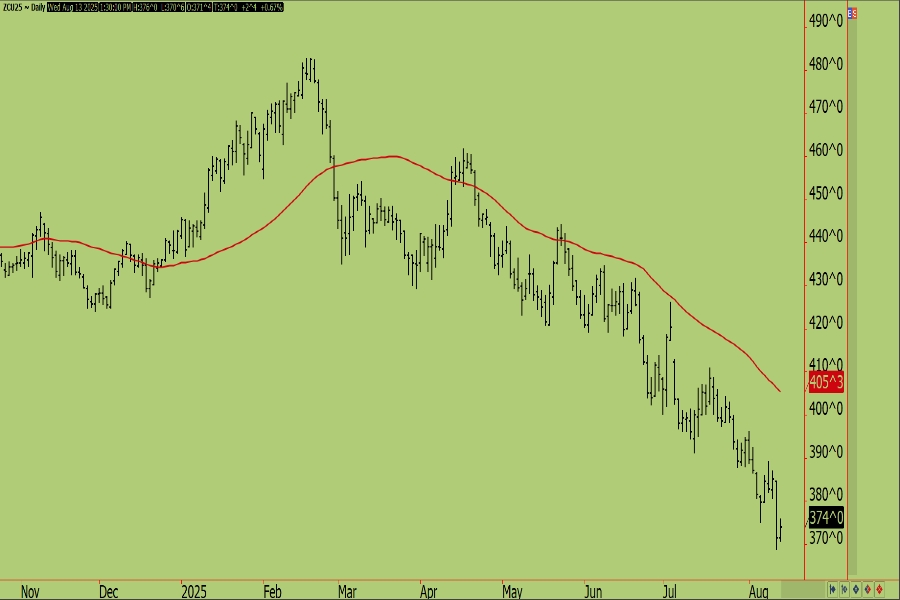

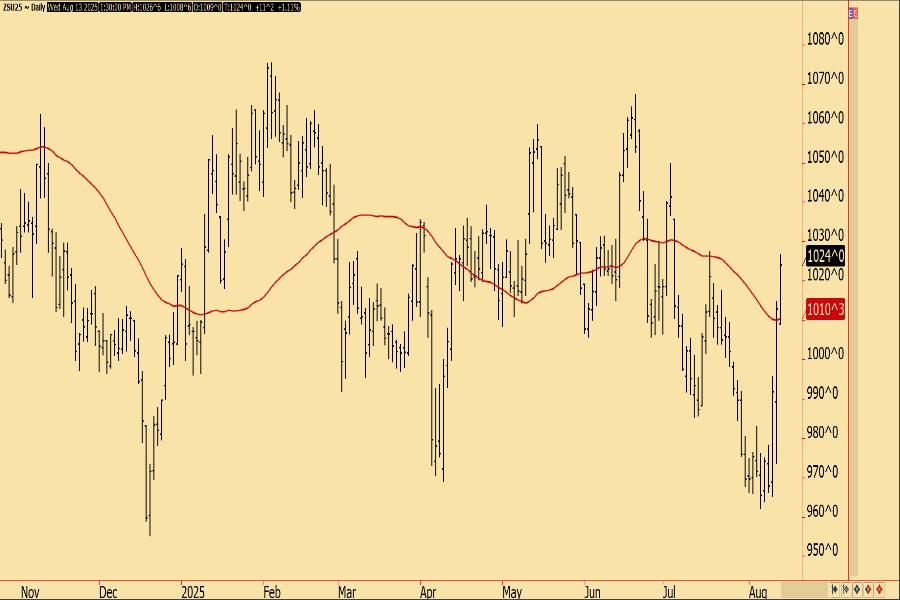

Soybean futures put in their third consecutive higher close on Wednesday this week and were able to drag corn and beans along with them as all three major US crop markets finished the day in the green. News-wise, a lot of the day's talking points continued to focus on fallout from yesterday's WASDE numbers, with there not being a lot otherwise for traders to sink their teeth into and short-covering due to the notable fundamental changes remaining one of the primary themes of the day. We mentioned it yesterday, but the soybean balance sheet needs Chinese demand and without it, current ending stocks numbers are likely on the low end, even with lower production.

|