|

? Prices:

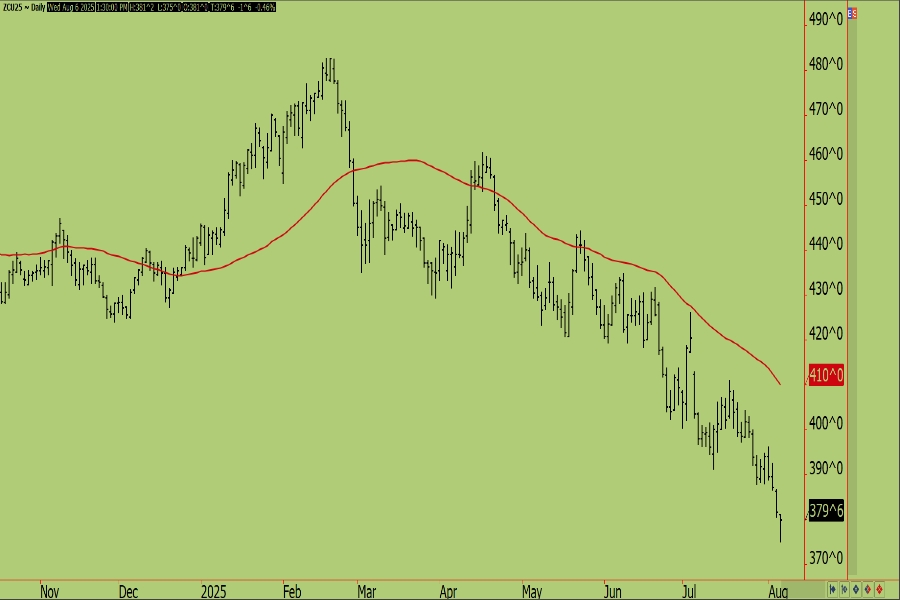

- September Corn (CU): $3.79 3/4, down 1 3/4 cents; new contract low at 3.75

- December Corn (CZ): $4.01 1/4, down 3/4 cent; new contract low at 3.96 3/4

- September/December Spread (CU/CZ): -21 1/2, down 1 cent

? Market Headlines:

- This morning's weekly ethanol update from the EIA missed the mark relative to trade expectations on both production and stocks for the week ending August 1st. The report showed average daily production in the week at 1.081 mil bbls/day, which was down 1.4% from last week and down 2.5% from the same week last year.

- Ethanol stocks in the week were down 4% from the week prior at 23.756 mil bbls and were down 1% from the same week last year.

- Corn usage in the week was estimated at 106.8 mil bu/day, which brings cumulative marketing year use to 5.086 bil bu.; this compares to 4.961 bil bu last year and the USDA's full marketing year forecast of 5.500 bil bu.

Summary:

New crop corn futures tested the $4 level on Wednesday before reversing course at mid-morning and finishing the day back above here as news remained slow for another session. Unless President Trump announces something positive on the trade front, which we are not overly optimistic about, we see it difficult for prices to make a bottom until more is known regarding crop size and just how big 2025/26 production will be, as this is pretty much all anyone cares about. There are demand questions as well going into harvest, mainly due to the size of the South American crop, but is the supply side that remains concern number one.

|