|

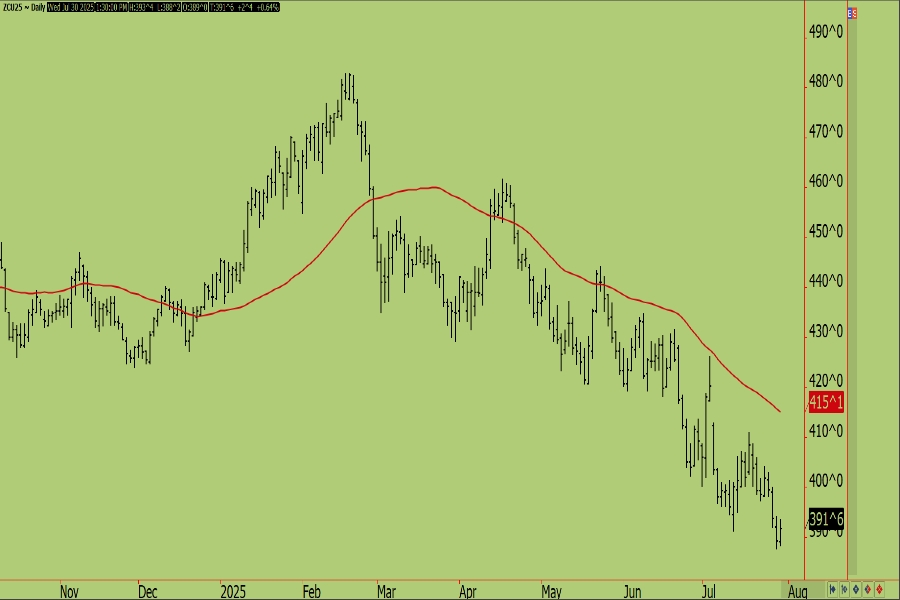

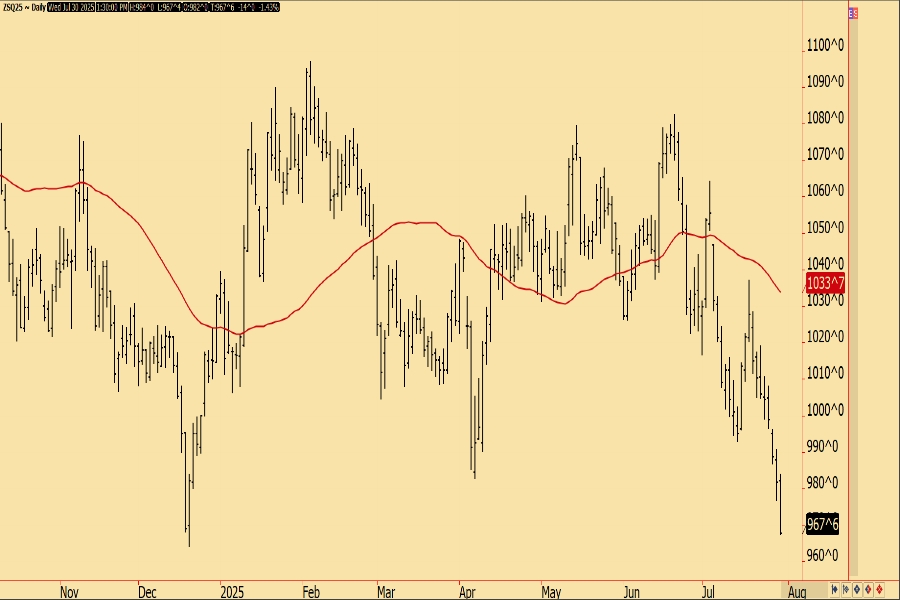

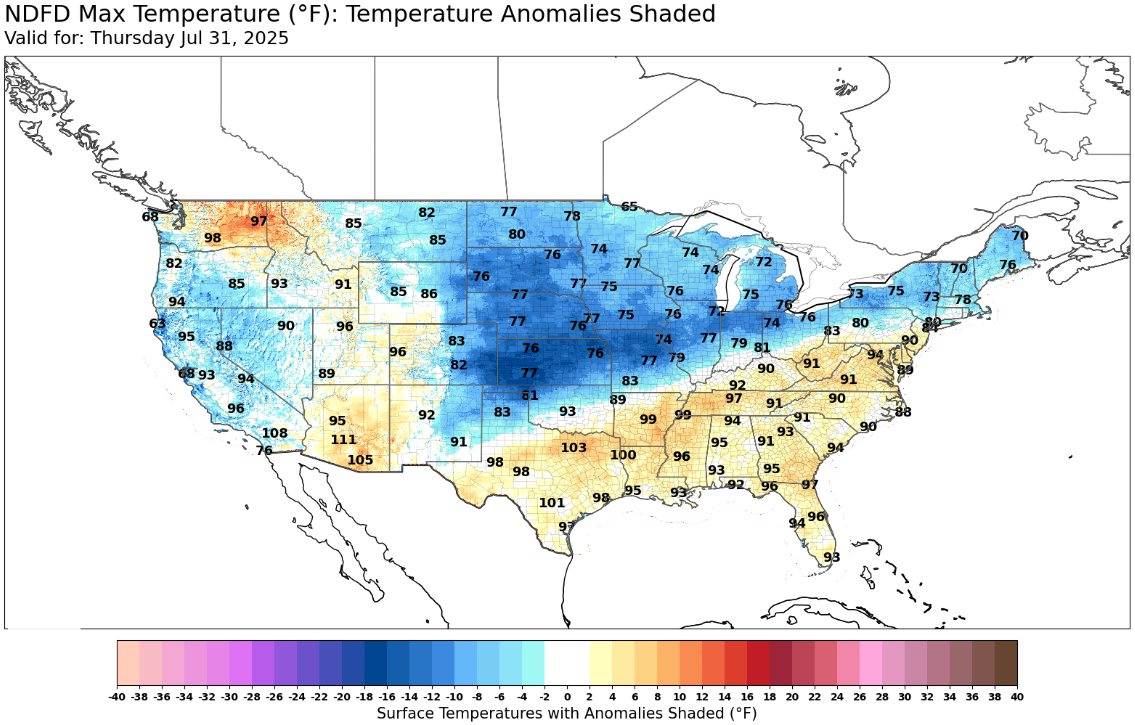

Corn futures ended their losing streak on Wednesday on an unwinding of spreads, but the rest of the space was unable to come along for the ride and again finished the day in the red as downward momentum continues to be the overarching theme in the market. News-wise, things continued to be much the same as previous days this week, with the ongoing mix of friendly weather forecasts, Trump tariff announcements, and large crop prospects continuing to dominate a lot of the daily headlines.

|