|

? Prices:

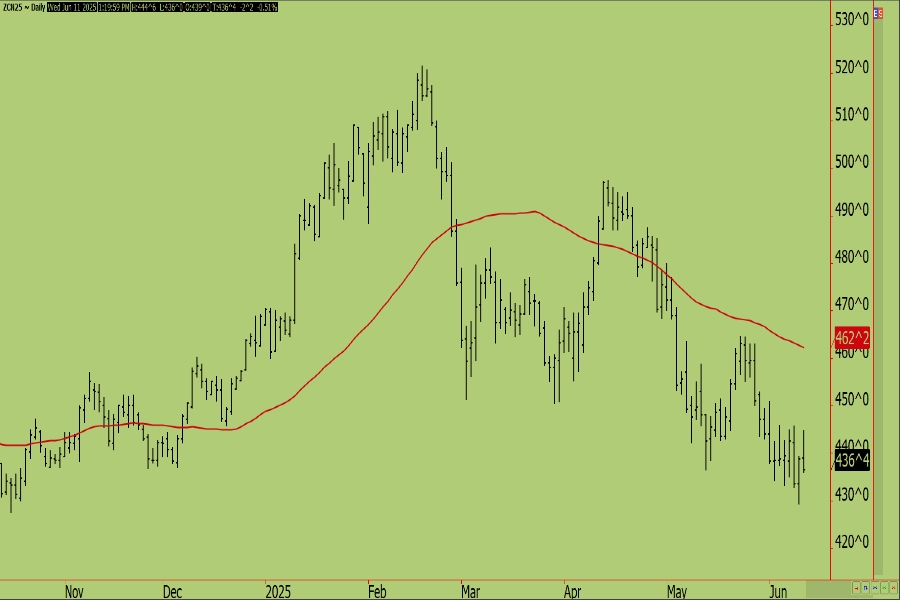

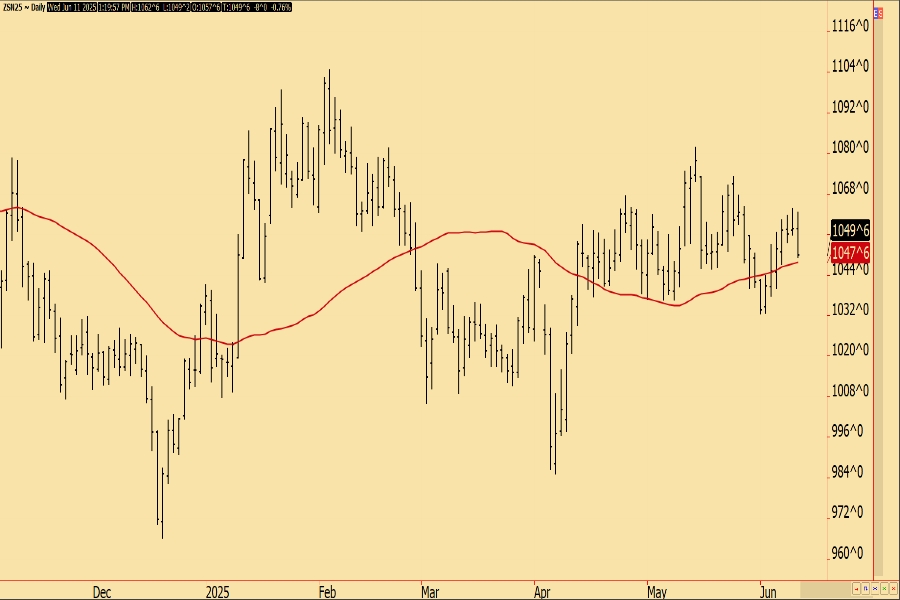

- July Soybeans (SN): $10.50 1/2, down 7 1/4 cents

- November Soybeans (SX): $10.29 1/4, down 2 cents

- July/August Spread (SN/SQ): 5, down 3 1/4 cents

? Market Headlines:

- Not a lot specifically new in the soy complex on Wednesday, as there is seemingly some measure of disappoint on the lack of explicit ag purchases in the rumored agreement between the US and China. The 10% tariff to remain in place applies to US soybeans and other ag products, which will significantly impact price competitiveness this fall.

- Traders see ending stocks in Thursday's June WASDE report at 351 mil bu in the old crop vs 350 mil last month, and see ending stocks at 298 mil bu in the new crop vs 295 mil last month. World stocks are seen increasing just marginally to 124.54 MMT's from 124.33 MMT's last month.

Summary:

Talk surrounding China continued to dominate the soybean market again on Wednesday, as traders were largely disappointed that a rumored framework agreement did not include any mention of fulfillment of the Phase One trade deal or any new purchases of US ag products, namely soybeans. Similar to corn, there aren't a lot of surprises expected out of either Conab or the USDA tomorrow, but the reports will at the very least likely take some of the headline attention off the trade situation for a bit.

|