|

? Prices:

- July Chicago Wheat (WN): $5.42, down 12 3/4 cents

- December Chicago Wheat (WZ): $5.79 1/4, down 10 1/2 cents

- July/September Spread WN/WU: -15, down 1 cent

? Market Headlines:

- Weekly wheat export inspections totaled 291k MT's, which was down 47% from the week prior. Cumulative inspections in the marketing year that began June 1 are seen at 168k MT's.

- China's 100% import tariff on Canadian canola has spurred a massive shift in planted area to more wheat, as growers turn to a crop that is less vulnerable to tariffs and other disruptions from the US or China.

- Private Black Sea Consultancy SovEcon on Monday raised their Russain wheat production estimate in the current season by 1.8 MMT's to 82.8 MMT's, citing good weather in the country's southern growing regions.

Summary:

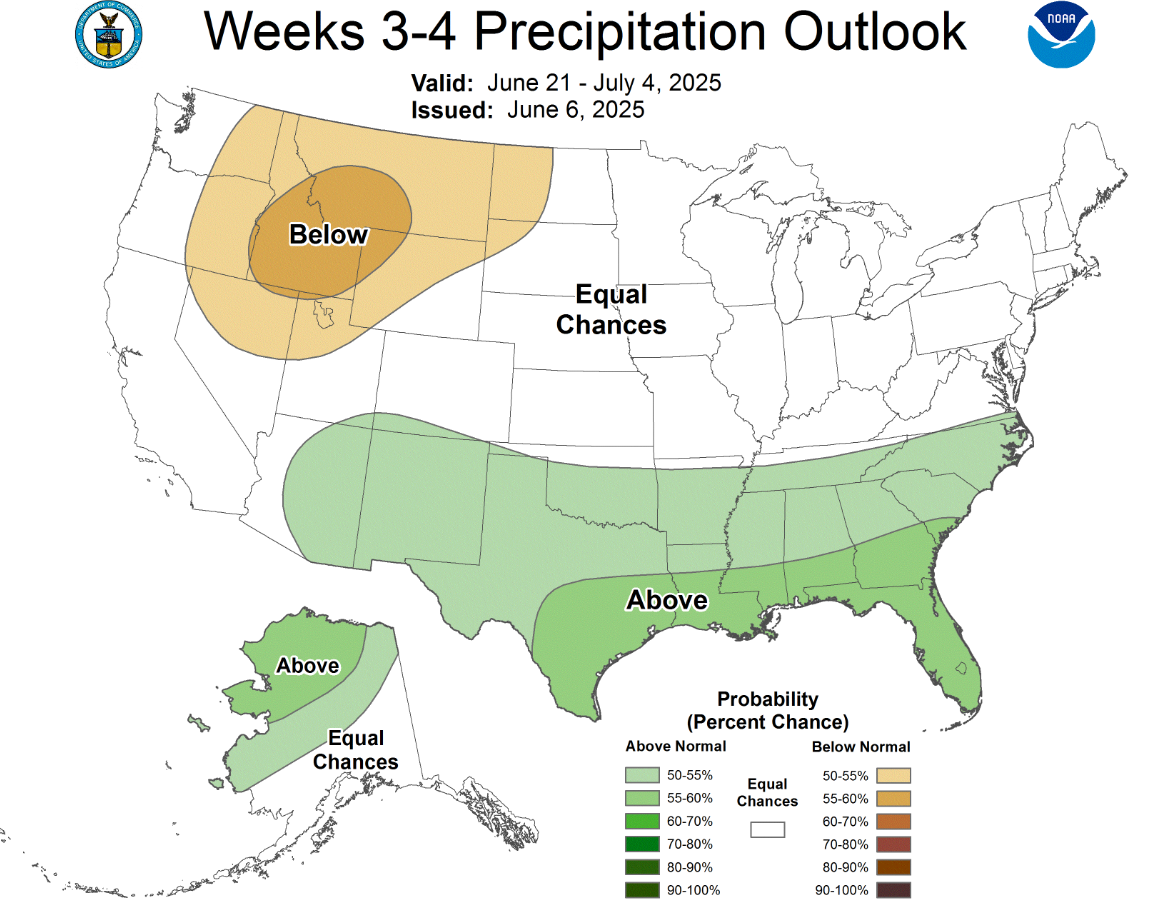

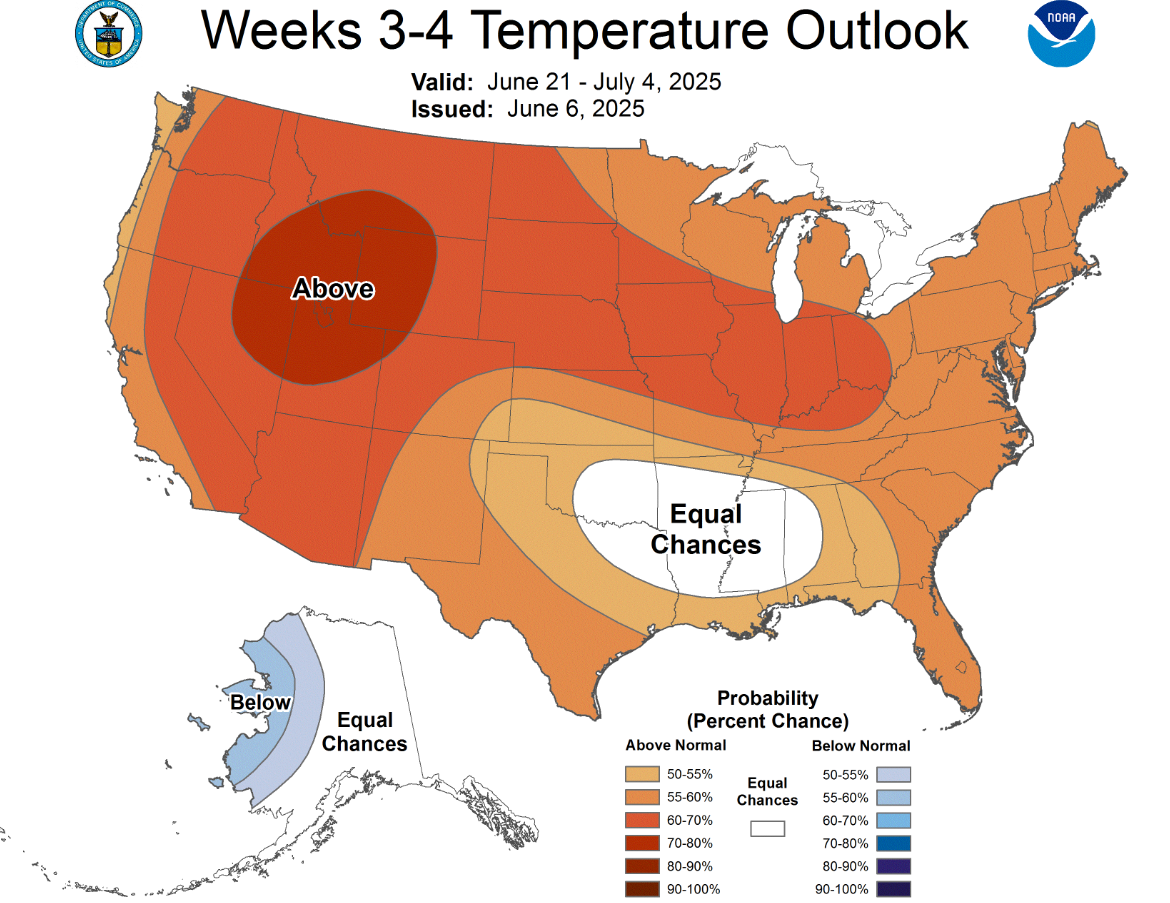

Wheat was generally considered the downside leader in the ag space Monday, as improving global weather, namely in the Black Sea, Canada and China, caused funds to continue to selling across all three markets. Harvest in the US is still a few weeks away for the most part, but this also looks to potentially pressure the market in the short term.

|